11 Notes on Amazon

The Family Papers #010

By Nicolas Colin (Co-Founder & Director) | The Family

Amazon is one of our favorite examples when it comes to explaining The Family’s investment thesis. It is one of the oldest digital companies around. And contrary to most of its peers, from the beginning it operated a business that included tangible assets (operating warehouses, delivering stuff) and lots of employees. Amazon, which is located in Seattle, was reportedly despised in Silicon Valley for that reason: why would an Entrepreneur even bother founding a low-margin, difficult-to-scale retail business when they could make tons of money in the ad-clicking industry?

Today, Amazon remains one of the most fascinating tech companies out there. It also sets an inspiring example for traditional brick-and-mortar companies that are looking to become more digital. If Amazon can operate a business model that is both digital and tangible, why can’t the US Postal Service or Air France-KLM?

The problem we encounter while trying to communicate our Amazon passion is that it inspires mistrust and hostility. “That is all very interesting, but why do they treat their employees so badly?” is a frequent reaction. “When will they post a profit, anyway?” is another. From union workers to corporate CFOs, everyone has good reasons to hate Amazon or, at the very least, to refuse to draw lessons from its success. So for all of you Amazon skeptics, below are 11 notes that could perhaps lead you to reconsider.

A Retailer Turned Technology Company

1/ When the tech bubble burst in 2000, it didn’t wipe out the whole digital economy. On the contrary, as explained by Carlota Perez and William Janeway, it marked the beginning of the deployment phase that has now seen digital companies enter industries such as healthcare, car manufacturing, energy and education. But the bubble was a tough time for companies that were operating at the time, especially if they had low margins. Amazon survived by laying off workers and cutting costs even more, but it was a wake-up call. Something had to be done to hedge against those low margins and to finally become a technology company.

According to Brad Stone’s The Everything Store, Tim O’Reilly provided Bezos with the solution. “Why not,” he essentially said, “open your infrastructure to harness user participation and enroll outsiders in the process of making the company more scalable?” That marked the day when Amazon entered the digital economy: not only using digital technology to take orders and process payment, but also leveraging it to make the whole business model create more value. The company’s marketplace for third-party sellers had been launched in November 2000. Amazon Web Services was envisioned in 2002. After turning its first quarterly profit in Q4 2001, Amazon finally broke even in 2003.

Meanwhile, the company’s engineering staff had apparently been killing itself to transform Amazon’s large IT infrastructure into a collection of Web services. It was not an easy task. In his now famous “Platform Rant”, former Amazon employee Steve Yegge detailed what it took for Amazon to deploy its current IT architecture. Everybody had to work incredibly hard to deploy the new Web services while ensuring continuity of operations. Multiple unexpected pitfalls were spotted along the way. The legendary and frightening Rick Dalzell, Amazon’s CIO at the time, had to whip everybody for years to make sure that the radical IT upheaval was achieved on time at a mastered cost.

Amazon succeeded where many others would have failed and it gained a lot in the process. Forcing each team to design its own Web service imposed a virtuous pressure that incentivized everyone to improve reliability and performance. The agility derived from using Web Services instead of integrated architecture made it easier to innovate and to A/B test many new features. Finally, the internal Web services used by Amazon itself were opened to outside customers in 2006, becoming Amazon Web Services, the company’s main driver of revenue. As suggested in Jeff Bezos’s 2010 letter to Amazon’s shareholders (a most rousing text about digital technology), Amazon has fully become a technology company.

Lower Prices v. Exceptional Experience

2/ A company is a contract between many parties. The value it creates is then distributed among its various stakeholders: its shareholders of course, but also its employees, executives, customers, creditors and suppliers. The more competitive the market is, the more value has to be distributed to the customers in the form of lower prices. This is what Sam Walton understood would help him turn Wal-Mart into one of the biggest corporations in the world. For a long time, Wal-Mart’s tagline read “Always Low Prices. Always.” Sam Walton meant it: each year, suppliers had to lower their price, or else they were out. And as related by Charles Fishman’s The Wal-Mart Effect, prices went down in Wal-Mart stores even in the absence of local competition.

Jeff Bezos understood something else that didn’t exist when Sam Walton operated his first stores in Arkansas: competition is even higher on digital markets. And his conclusion was not that you should drop the prices even lower than Wal-Mart ever did: if Amazon had done that it would have disappeared just as many — among them Thomas Friedman— predicted it would. Bezos concluded that the only way to retain customers without bringing down the prices was to provide an exceptional customer experience.

Amazon has accordingly set a new standard. It has extended the experience it provides to the customer far beyond the transaction, building one of the most powerful closed ecosystems of the digital economy. You can now buy almost everything on Amazon, even from third-party sellers; you can find inspiration; you can watch movies; you can read e-books on a device that is provided by Amazon; now you can even book home services. And the more you rely on Amazon for your day-to-day life, the more difficult it becomes to even consider offers by Amazon’s competitors. Of course, you can compare prices whenever you have something to buy. But saving a few cents here and there may not be enough to compensate for the effort that it takes to go browse prices all over the Internet. In fact, Amazon proves that you can design an experience that invites customers to simply trust the company over the long term instead of constantly evaluating the competition.

This is one key to understanding Amazon. There are many detractors willing to say bad things about Amazon. But any criticism about Amazon lowering prices doesn’t stand, since Amazon is not about lower prices. Pricing the Wal-Mart way was dominated by economies of scale: the higher the volume, the lower the cost, and the price. In the digital economy, it’s different. In a business driven by increasing returns, there will always be new entrants willing to lose money on certain goods if only to monetize later or elsewhere in their business model. Replicating Wal-Mart’s strategy in the digital economy would be suicidal.

Above all, prices can evolve in real-time, and new pricing strategies can now be devised that are radically different from the ones we were used to in the Fordist economy. Operating a digital business enables one to monitor what happens in the entire business and use machine-learning algorithms to predict how money can be made later even though prices are currently low. As pointed out by David Streifeld a few years ago, prices on Amazon are a mystery and they change fast. In some cases, digital companies can even raise the prices as the volume goes up, because other incentives will inspire customers to buy anyway: those could be peer pressure and virality on social networking platforms, or… an exceptional user experience.

The Architecture of Participation

3/ It takes several steps for an industry to go digital. The first step is when startups begin to multiply and try to test new ways of doing business. The last step is when one of these startups, having formed an alliance with hundreds of millions of users, has taken over the entire industry, evicting or commoditizing every established company in the process. At every step, what the incumbent companies tend to express is denial.

When traditional chain store retailers consider Amazon, the expression of denial usually consists in declaring that Amazon and traditional retailers essentially do the same business, with only tiny differences of no importance. To be frank, we all have the same bias: when someone vaguely resembles you, you tend to concentrate your attention on similarities instead of focusing on the differences. But in the case of Amazon and traditional retailers, it really is the differences that matter.

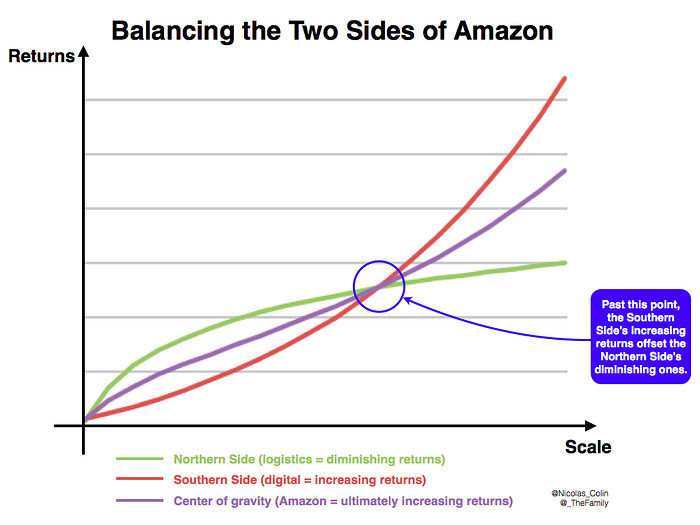

Because of that familiarity bias, when they look at Amazon, traditional retailers only see what I call the Northern Side: operating a massive logistics infrastructure, negotiating with suppliers, delivering products to customers as mail-order businesses have been doing for a very long time. All these various businesses, combined in a traditional retailer’s business model, imply diminishing returns: the more you grow, the more you have to pay to convert and serve additional customers. As a result, the retail sector is usually dominated by oligopolies — such as the one formed in France by Carrefour, Casino, Auchan, E. Leclerc, and others. When a company reaches a larger scale of operations in such a business, its logistics infrastructure is so huge and the employees are so numerous that, as author Matt Dickinson wrote about the North Face of the Everest, “a simple slip would mean death.”

This is the reason why traditional retailers prefer to stop growing at some point and why they’re convinced that Amazon will ultimately crash when it passes that point. But what those old retail professionals are missing is Amazon’s other side, the Southern Side, on which the company has deployed Tim O’Reilly’s famous “Architecture of Participation”, thus making the most of digital technologies by harnessing the power of its users to create even more value. As O’Reilly wrote in 2004 in his masterful article “Open Source Paradigm Shift”,

Products identical to those Amazon sells are available from other vendors. Yet Amazon seems to enjoy an order-of-magnitude advantage over those other vendors. Why? Perhaps it is merely better execution, better pricing, better service, better branding. But one clear differentiator is the superior way that Amazon has leveraged its user community…

Amazon doesn’t have a natural network-effect advantage like eBay, but they’ve built one by architecting their site for user participation. Everything from user reviews, alternative product recommendations, ListMania, and the Associates program, which allows users to earn commissions for recommending books, encourages users to collaborate in enhancing the site. Amazon Web Services, introduced in 2001, take the story even further, allowing users to build alternate interfaces and specialized shopping experiences (as well as other unexpected applications) using Amazon’s data and commerce engine as a back end.

While returns are clearly diminishing on the Northern Side, the opposite trend — increasing returns — is at work on the Southern Side. For Amazon, every new warehouse costs more than the previous one, especially because it has to be located closer to the city so as to shorten delivery time (= diminishing returns). But the new customers that this warehouse will enable Amazon to serve will drive more than revenue: as they join the experience made possible by the architecture of participation on the Southern Side, they create value for Amazon through many channels: revenue, higher volumes, network effects, machine learning, and content-driven virality (= increasing returns).

Life is very different on the Southern Side as compared to the Northern Side. On the North Face of the Everest, the higher you climb, the more painful it gets. On the Southern Side, however, increasing returns radically change the rules of the game: the higher you climb, the easier it gets (and thus the faster you run up to the peak). Additionally, unlike on the Northern Side, you can slip on the Southern Side without that simple slip meaning death. Here, even failures generate valuable data that can be put to work to improve the customer experience: as Justin Fox reminds us in Harvard Business Review, “an apparent failure like the Amazon Fire phone can be treated as a learning experience rather than a crisis.”

Thus another key to understanding Amazon’s business model is that precarious balance between the Northern Side and the Southern Side: as long as returns increase more on the Southern Side than they diminish on the Northern side, Amazon can open many new, costlier warehouses and create even more value for its growing user community. I have no insight into this, but somehow I’m convinced that every night and every morning, Jeff Bezos glances at some dashboard just to check that the Southern Side weighs more than the Northern Side — which means that the company, even if it’s already so large, can continue to sustain its growth with (slightly) increasing returns. That would mean Bezos actually manages Amazon’s increasing returns, as envisioned by Michael Schrage in this Harvard Business Review article: “Effectively managing the network effects portfolio will become one of the most important challenges tomorrow’s management will confront.”

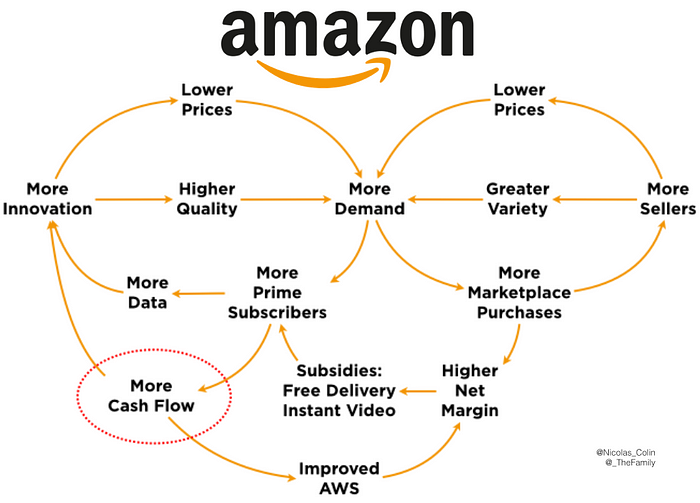

Finally, participation does not only serve the goal of improving the experience at the margins and making customers more loyal; it also empowers the users within the supply chain to take control and help make Amazon more scalable. It may even explain Amazon’s work culture. You’d think that user participation is the exclusive mark of nice companies. You’re wrong: imagine thousands of impatient, whimsical bullies storming in the factory and telling the workers to serve them better and to hurry up. This pressure from the customers, amplified by Bezos’s obsession with serving them better, explains why it apparently is so hard to work at Amazon, both on the Northern Side (= the pressured workers in the ever-more-efficient warehouses) and on the Southern Side (= the software and marketing folks constantly evaluated on their capacity to enhance user participation).

Prime At The Core

4/ Amazon seems very far away from the sharing economy. It doesn’t mean that user interactions are of a lesser importance. Quite the contrary: there are so many opportunities for Amazon users to interact with one another, from customer reviews to recommendations, not to mention the affiliate program and, of course, the marketplace. In truth, even though Amazon doesn’t stress that point in its communication, it really is as user-driven as other Web 2.0 businesses such as YouTube, Airbnb, or Wikipedia. Indeed, Amazon became a platform long before the term made its way into mainstream media.

As you can learn in politics (and by reading authors like Saul Alinsky), the key to sustaining a vibrant and growing user community on a digital platform is to cater to the power users — those who belong to the vanguard and use the product the most. Power users may not be the ones who spend the most on the platform, but their individual spending multiplies many times over because they reveal emerging trends and they talk a lot about what they do on the platform. As a result, they create value on every side of the business model: they inspire other users to spend more, and they help the company and its suppliers reach better decisions when it comes to allocating resources and setting prices.

Prime is designed for Amazon’s power users. As such, it serves many purposes. Like coupons, it enables Amazon to detect those among its customers who are really attached to having their goods delivered the next day for no additional cost. Once they’re revealed by their Prime subscription, Amazon is able to redeploy its resources and concentrate its next-day (and more and more same-day) delivery efforts on Prime subscribers, if only to keep them satisfied. Also, as the unit cost of delivery has been converted into a yearly subscription, a major source of friction has been removed and Prime subscribers can begin ordering goods on impulse, and not think twice. Hence it helps reveal what people want, almost in real time, which generates useful data flows from which Amazon can extrapolate larger market trends. Thanks to its Prime subscribers, Amazon can reach higher volumes, achieve much-needed economies of scale and increase its market power over suppliers.

This is precisely why Prime is a key component of Amazon’s business model: it was launched to detect and attract Amazon’s power users, and to nurture them. The improved features and exclusive offers could then be leveraged to make the rest of the business grow further. In a thoughtful article published last year on Wired, Marcus Wohlsen dubbed Prime “one of the most bizarre good business ideas ever,” discussed Prime economics in great detail and rightfully concluded that “Prime’s seemingly random hodgepodge is, it turns out, a finely tuned engine that drives the consumption of physical and digital goods in a seemingly unstoppable cycle optimized for the 21st-century economy.”

Those Low Margins

5/ Ah, the curse of consumer markets. Consumers are merciless, ready to deprive a company of its profit, even to force it into bankruptcy, if it’s the only way for them to obtain lower prices. This was not obvious before the advent of the Internet, because then-dominant companies defended themselves with high barriers to entry to prevent competition from bringing prices down. But in the digital economy, barriers to entry are much more difficult to erect. As a result, no company wants to be on its own facing consumers: if it does, chances are high that it will soon see its margins squeezed because of the necessity to keep on lowering prices.

Why, then, are consumer companies so dominant in the digital economy? The reason is that it is so difficult to scale up operations selling to business customers. As written in a previous issue, “enterprise markets may be a trap: FedEx sells to companies because it’s expensive (no ordinary individual can pay for it on a regular basis); and it’s expensive because its scalability is limited by the absence of user participation on an enterprise market.” This is why there are very few giant, fast-growing tech companies that are 100% old-style enterprise when it comes to selling: Palantir Technologies comes to mind as a rare exception.

To conquer enterprise markets, some enterprise companies behave as if they’re on a consumer market, even though they sell to businesses: Slack is a good example. Others, such as Google or Facebook, occupy the sweetest spots in the digital world. They have formed a strong alliance with billions of individuals, harnessing their power to sustain increasing returns, and yet they sell to business customers which are more prone to leaving a producer surplus on the table, for two reasons: businesses can cover the spending with superior earnings, and businesses are oftentimes suckers when it comes to buying—as observed by Paul Graham: “A large part of what big companies pay extra for is the cost of selling expensive things to them.”

Those enterprise exceptions are so rare, because of the difficulty to scale up on enterprise markets, that many Empire builders, among them Jeff Bezos, have to deal with the curse of consumer markets. The way to survive that curse is either to remain confined on a high-end segment (= Apple) or… to live with low margins (= Amazon). In other words, the fact that Amazon never made a profit is not because, as Matthew Yglesias once put it, “it is a charitable organization being run by elements of the investment community for the benefit of consumers.” Rather, it is because the only ways to keep on growing on a consumer market are to create an exceptional customer experience, to use superior growth as a barrier to entry, and to live on low margins.

Eugene Wei, one of the most inspiring writers on Amazon, explains it in a more figurative way:

A profitless business model is one in which it costs you $2 to make a glass of lemonade but you have to sell it for $1 a glass at your lemonade stand. But if you sell a glass of lemonade for $2 and it only costs you $1 to make it, and you decide business is so great you’re going to build a lemonade stand on every street corner in the world so you can eventually afford to move humanity into outer space or buy a newspaper in your spare time, and that requires you to invest all your profits in buying up some lemon fields and timber to set up lemonade franchises on every street corner, that sounds like a many things to me, but it doesn’t sound like a charitable organization.

Finally, margins also derive from a company’s culture, not necessarily from the industry in which it operates or the market it serves. Apple prefers high margins, and they’re willing to sacrifice market share to get them. Amazon prefers low margins. It is easy to go from high to low margins: that happens if a company gets dragged into a competition for lower prices. But it is equally easy to go from low to high margins—and it is also very dangerous, because not only does it mean that you have to sacrifice growth, it doesn’t fit in the company’s culture: thus it makes people complacent and there is no way back.

Refusing to renounce low margins even though there have been many opportunities to do so is probably one of Jeff Bezos’s most impressive achievements to date. As Eugene Wei suggested in another post, Amazon favors low margins so as to suck all the air out of the room and thus make its competitors suffocate. Hence those low margins are not a liability. Rather they are Amazon’s most potent comparative advantage.

Loosely Coupled Business Models

6/ Last year, I had the opportunity to meet with an executive of Vinci, a giant public French corporation that does business in both construction and the utility sector (mostly conceded highways and airports).

He explained that Vinci’s dual business model had been designed for financial reasons. Construction is a low-margin business that employs little capital; but it generates massive amounts of free cash flow thanks to a low cash conversion cycle(construction contractors take their time in paying their suppliers). On the other side of Vinci’s business model, utilities are very demanding in terms of investment and accordingly employ a lot of capital throughout very long investment cycles (sometimes decades); but in time they generate substantial net income that, ultimately, makes most of Vinci’s profits and dividends. All in all, the two businesses are complementary: without the construction business, it would be very difficult for Vinci to invest in its utility infrastructures, lest they bear the risk of excessive leverage; and without the concession business, Vinci would be incapable of turning substantial profits for its shareholders.

Amazon, like Vinci, has a complex, pluralized business model that is tied together mostly by sophisticated financial engineering. There are many things that we don’t know, but we can guess about a great deal.

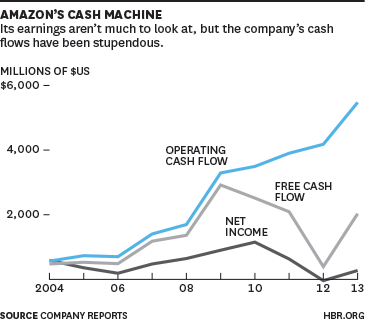

As shown by this graph, the absence of profit doesn’t mean that Amazon doesn’t generate cash flow. In fact, as Justin Foxwrote two years ago in theHarvard Business Review, “all that cash flowing in and sticking around a while before it has to go back out again makes it possible for the company to undertake experiments, learn from mistakes, and keep plowing ahead regardless of what those on the outside (such as shareholders) think.”

For instance, when it sells from its own inventory, Amazon doesn’t generate margins, but it surely does generate operating cash flow… and lots of data — because Amazon, not a third party, is the seller, it knows everything about both the customer and the transaction. That operating cash flow can then be allocated to capital expenditures, operating expenditures, and lowering the price of certain products. And all those allocation decisions are driven by the available data. One of the consequences is a better customer experience, which in turn generates higher liquidity on the marketplace where products are sold by third-party sellers. And on this marketplace, margins are higher for Amazon than when it sells from its own inventory, which secures the possibility for Amazon to generate net income in proportions high enough to reassure its shareholders.

All in all, without Amazon’s own inventory (and the cash flow it generates at the expense of suppliers), it would be very difficult to invest in and improve the customer experience, since they would constantly need to raise more cash; and without the marketplace, Amazon would be incapable of maintaining its profits and losses above the waterline. Amazon’s own retail business and the marketplace are loosely coupled, complementary businesses that enable sophisticated financial engineering dedicated to growth.

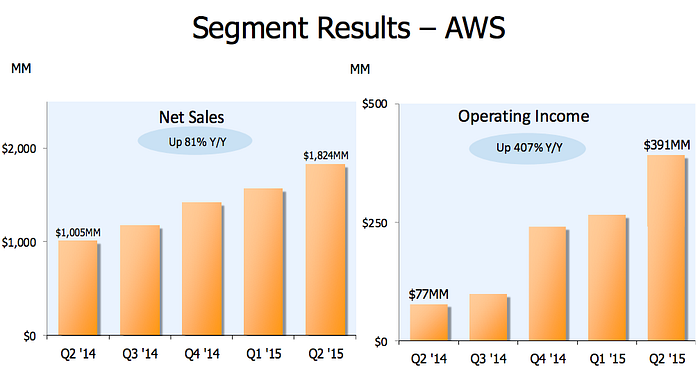

On top of that, there is Amazon Web Services, whose growth rates and profit margins are significantly higher than those in the retail part of Amazon’s business. The exponential growth of Amazon’s impressive cloud computing platform inspires positive feelings in investors (although there aredissenters): it is seen as both a growth driver and a way to escape the curse of consumer markets and finally make a profit (8% of sales, but 52% of operating profit).

Obviously, this doesn’t mean that Amazon is prepared to leave the retail business anytime soon. Instead, it can keep on improving its AWS offer and lower its price precisely because it serves the general public through its retail business. In other words, AWS is better because it is operatedunder the pressure of Amazon serving its own retail customers. This is what IT people call “dogfooding”: serving individual customers on top of AWS instead of only providing AWS to other businesses helps reveal the secrets Amazon could otherwise not see — what cloud computing resources it takes to operate a consumer digital business at a very large scale.

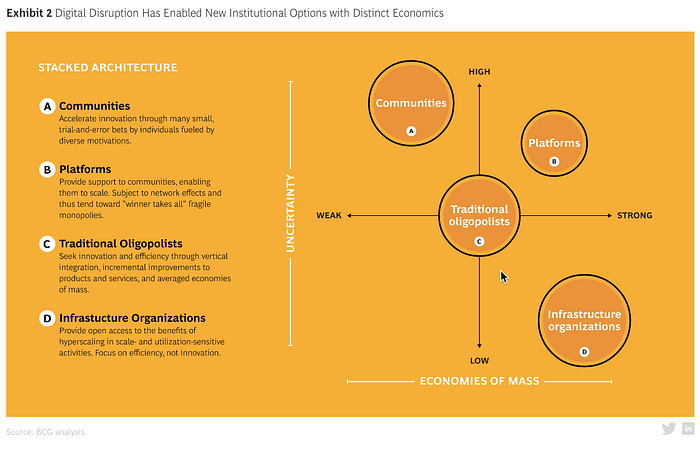

There are many ties between Amazon’s different businesses. Like Vinci, operating several businesses with very different financial metrics enables Amazon to summon sophisticated financial engineering to make its low margins and exponential growth sustainable. But, as proved by the ‘dogfooding’ approach to AWS, the various businesses also serve as checks and balances for one another, thus enabling Amazon to improve operational performances of every line of business under pressure from the other parts of the system. In the very useful framework designed by Philip Evans and Patrick Forth of the Boston Consulting Group, Amazon checks every box: it’s an infrastructure organization (AWS and Fulfillment by Amazon), a traditional oligopolist (Amazon the retailer), a platform (the marketplace), and it has formed a strong alliance with a vibrant community thanks to the O’Reilly-inspired“architecture of participation” (see part 1). As Evans and Forth write,

Amazon is now run as four loosely coupled platforms, three of which are profit centers: a community host, supported by an online shop, supported by a logistics system, supported by data services. Unlike many of his rivals, Bezos saw business architecture as a strategic variable, not a given. He did not harness technology to the imperatives of his business model; he adapted his business model to the possibilities — and the imperatives — of technology.

We’re slowly leaving that world dominated by business consultants and financial markets, in which it was so important to focus on one’s core business. On the contrary, the new conglomerates prove that it has become critical to diversify business models for at least three reasons:

- first, you have to retain your customers with an exceptional experience, which means that sooner or later you’ll have to enclose your ecosystem with more and more products integrated into an exceptional, ever-improving experience. In that matter, delivery is Amazon’s next frontier, and many signals suggest that it will soon tie delivery services to its model instead of outsourcing them to UPS, FedEx, and postal services all around the world;

- second, it is also important to operate not only different businesses, but also different revenue models. To hedge against risk and especially cyclical variations, it certainly helps to have different income and expenditure models in your portfolio: for instance, Amazon Web Services is a fixed-cost, high marginal revenue business, whereas selling goods has a higher marginal cost (notably because of the delivery costs and the cost of sales);

- third, as the digital economy is so volatile, you never know what may happen to your core business: thus non-core businesses are both growth drivers and fallbacks in case the company is having a bad day on its core business. Google is obviously worried about what may become of its sponsored links-clicking business, hence Google X and now Alphabet.

Domesticated Investors

7/ There isn’t really a need to retell the amazing story of Amazon’s relationship with its investors. Justin Fox has done it in this remarkable piece published by the Harvard Business Review in which he reminds us that Jeff Bezos is “a hedge fund veteran who has always taken a skeptical view of Wall Street, treating it more as a loopy rich uncle than the efficient information processor of standard finance theory.” A few things, though, should be stressed.

First, even though it’s already a very large company, Amazon should still be growing for a long time to come: that’s because it only controls a quarter of the online retail market (in the US), and online sales only represent less than 10% of the retail market as a whole. That leaves Amazon with plenty of terrain to conquer, all the more so because it is driven by its (slightly) increasing returns (see part 1) and can thus bear the weight of growing even larger. So its investors are not even close to seeing Amazon turn a stable profit. And if (when) Amazon does peak one day, it won’t be the end of the story: competitive pressure (by traditional retailers such as Wal-Mart, or by Chinese competitors such as Alibaba) will still make it very hard to reward investors with sizable profits, let alone dividends. Ultimately, Amazon will have to continue to grow, even though it means expanding its global operations, launching new products, or becoming an even bigger platform for third-party sellers and developers.

Second, most people know that Jeff Bezos insisted on the long term in theletter issued in 1997 when the company went public. Bezos proved he had already understood a very important constraint that didn’t exist before: in the digital economy, the various stakeholders cannot be confined to parallel universes. As a result, it is no longer possible to communicate through separate channels with stakeholders so diverse and with interests so divergent as employees, shareholders, and customers. Pre-digital CEOs could have it every way: saying that their priority was to create value for shareholders, but also that the customer was king, and of course that the employees were the company’s most precious asset. Every one of those conflicting constituencies could very well have the impression that it was at the top of the CEO’s mind.

But today, if you communicate about shareholder value the same way that CEOs like Boeing’s Phil Condit did 20 years ago, this might come to the attention of your customers, who are super-informed and hyper-sensitive as to how you’re willing to treat them; and the CEO best beware if they become convinced that they’re not your priority and that you prefer cater to the financial markets. This is why Bezos’s authority over Amazon’s shareholders is a crucial contribution to his forming Amazon’s impressive alliance with its customers. When an Amazon customer hears that the company doesn’t turn a profit and that it makes its shareholders run screaming, it inspires customer trust: that means Amazon isn’t taking money out of their hides and that customers are really guaranteed to have the best deals if they choose Amazon (meanwhile, Wal-Mart pays a $7B-a-year dividend to its shareholders).

The customer’s point of view is actually embedded in many parts of Amazon’s culture and operations. According to Brad Stone’s The Everything Store, all external communication, including that of the company towards investors, are made as if they’ll ultimately be read by the customers — which they eventually are. Also, all internal documents tend to be written from the customer’s point of view, which helps Amazon making decision-making more efficient. Quite simply, focusing on the customer is Amazon’s big idea: it helps in making decisions in the face of urgency (“Is it in the customer’s best interest?”), and it attracts the superfans the company needs to make its user community more engaged.

Lastly, Amazon’s relationship with its shareholders could very well foreshadow the future of stock markets in general. Stock investment strategies have traditionally been organized around the basic division between growth stocks, value stocks, and income stocks. The expectation of investors used to be that, in due time, every growth stock would become an income stock. What we are seeing clearly now is two unprecedented phenomena.

The first phenomenon is that digital companies seem to never become income stocks. They may turn huge profits and have cash stockpiles in Bermuda or in the Cayman Islands, like Apple or Google, but mostly they stilldon’t pay dividends to their shareholders (with rare exceptions). Apart from the highly technical tax reasons (you can read all about the ‘check-the-box’ regulation here), the reasons why digital companies don’t pay dividends are simple enough: they have to keep on growing as a critical condition of survival, they like to keep their war chest intact in case they have to react to an unexpected threat, and they want to continue to appear as if they’re an innovative technology company dedicated to improving their customers’ experience instead of focusing on shareholder value. As Peter Thiel declared when debating Google Executive Chairman Eric Schmidt a few years ago,

Google is no longer a technology company, it’s a search engine. The search technology was developed a decade ago. It’s a bet that there will be no one else who will come up with a better search technology. So, you invest in Google, because you’re betting against technological innovation in search. And it’s like a bank that generates enormous cash flows every year, but you can’t issue a dividend, because the day you take that $30 billion and send it back to people you’re admitting that you’re no longer a technology company. That’s why Microsoft can’t return its money. That’s why all these companies are building up hordes of cash, because they don’t know what to do with it, but they don’t want to admit they’re no longer tech companies.

This is why public digital companies are so reluctant to provide the market (and the tax authorities) with detailed information about their finances and operations. As Eugene Wei mentioned in one of his great articles about Amazon,

“Tech companies, in general, have dealt with the press, investors, and public long enough now to have decided that for the most part, disclosing less buys them the most strategic flexibility with the least amount of pain. Tech companies have an interesting ambivalence towards the public capital markets. They rebel against resource dependence theory because they don’t believe their investors know how to run their businesses better than they do, but on the other hand, being public is a great boon to compensating knowledge workers who have a lot of job options.”

The second phenomenon is that traditional companies that refuse to become digital will have a hard time continuing to turn sizable profits and will be less and less able to guarantee a steady dividend — hell, like Kodak, they could even face the ungrateful fate of bankruptcy. This all means that stock market investors will have to begin to act like venture capitalists, even though they’re investing in liquid stocks on the public market. Like venture capitalists, they will have to learn to make their earnings with mostly capital gains instead of dividends (beware, then, theweakening of carried interest). And like venture capitalists, they will have to learn to accept losing money on a lot of portfolio lines, if only to win even more money with the few remaining lines that will be exponentially successful. So far, Amazon has been one of these. And this is why Jeff Bezos has managed to keep those investors at a distance.

Being the Leader

8/ Most people mistake the digital economy for one in which the first mover has an advantage. Companies like Google and Amazon are so large and have inspired such a high level of trust in their users that it seems impossible for new entrants to break into the market. Hence the impression of a first-mover advantage: those giant companies were there first; they seized all available dominant positions; now they’re unbreakable.

Nothing could be further from the truth. In reality, the digital economy is governed by another rule, that of winner-takes-all (or winner-takes-most, as Fred Wilson recently put it), which is very different from that of the first mover advantage. In truth, on most markets, the winner is far from being the first mover. Before Facebook, there was Friendster and Myspace. Before Google, there were forgotten search engines such as Lycos, Altavista, or even Yahoo. Before Amazon, though, there was… not much.

This is where Jeff Bezos really stands as an outlier. As George Packer wrote in The New Yorker, he had the insight to surmise that selling books first was the pathway to global domination in retail. It has long topped European online retailers, which once thought they had a sustainable advantage over their US counterparts since Silicon Valley was so uninterested in the retail business. Today, Amazon remains miles ahead of the U.S. competition in the online retail space. According to data from e-commerce research firm Internet Retailer, Amazon’s online retail sales amounted to $67.9B in 2013, more than the next 9 largest e-retailers combined, including large traditional retailers such as Wal-Mart or Staples. And this isn’t going to change anytime soon. As former Fab CEO Jason Goldberg recently reminded us, quoting Jason Del Rey ofRecode,

Amazon accounts for half of all sales growth in U.S. e-commerce, meaningonline retailers not named Amazon are battling for around 50 cents of every new $1 spent online. As if that weren’t enough, Amazon also accounts for about a quarter of every new $1 of growth in all of retail, including brick-and-mortar sales, too.

Being the leader makes a singular company out of Amazon, since on a winner-takes-most market, the leader’s strategy cannot be analyzed within the same framework as its challengers. Being the leader empowers Amazon on various fronts.

First, being the leader makes it easier to create and sustain an exceptional customer experience through increasing returns. This is precisely why the digital economy attracts exceptional Entrepreneurs such as Jeff Bezos, because increasing returns makes it possible for companies to reach a dominant position in which, in Babak Nivi’s enlightening words, “there is no tradeoff between quality and scale.”

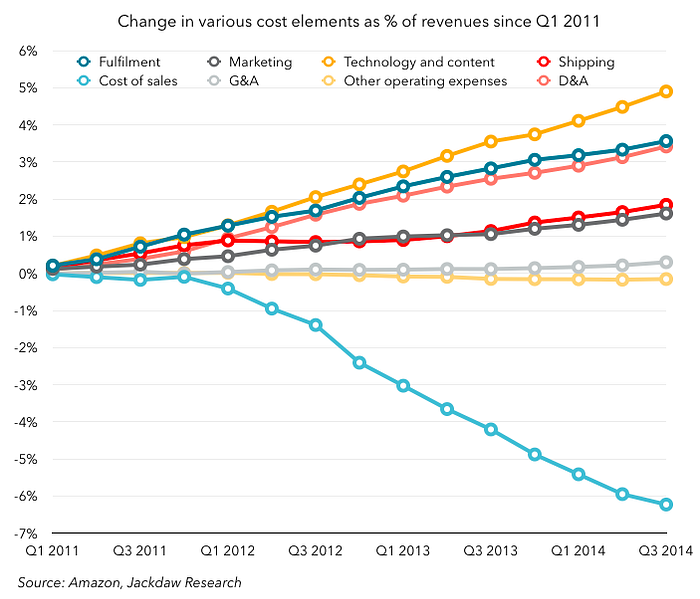

Second, on a retail market in which relationships with suppliers are key to making the business sustainable, being the leader enables Amazon to buy higher volumes and thus to obtain lower prices. As shown by this graph about Amazon’s evolving cost elements, the company’s cost of sales has plummeted as a percentage of revenues since Q1 2011.

Third, being the leader also enables Amazon to turn threats into opportunities. This is particularly obvious when it comes to taxes. As related in a recent issue of the Financial Times, the new obligation to collect sales tax based on delivery address instead of permanent establishment could have been a major blowback to Amazon; instead, it seized this adverse policy as an opportunity to widen the reach of its distribution network and to increase its lead over its challengers:

Amazon’s push to locate more infrastructure close to consumers is also linked to a gradual change in US tax rules. When Amazon first started selling books, most US states did not collect taxes on items that were shipped from another state, prompting the company to build giant warehouses in states with low or no sales tax. The rules have largely changed. Roughly half of US states now collect sales tax based on delivery address, removing the advantage of sourcing from an out-of-state warehouse. Amazon has been building out a new network of midsized distribution centres, or “sortation centres”, that act as a staging ground between the mega-warehouses and local post offices.

Finally, being the leader is what really makes the difference for investors. It obviously is easier to serve your customers before your own investors if you can present the latter with superior performances. If the winner takes all (or at least takes most), then being an investor in the leader is accepting the promise of being rewarded with substantial returns as the stock continues to gain traction.

Will Amazon remain the leader? Every tech giant has now expressed an interest in either retail or delivery or both: on paper, Uber, Google, Apple, and even Facebook (through payments) could end up being direct competitors to Amazon. Formidable rivals such as Alibaba are also emerging from other continents. New ambitious entrants, such as Jet, seem to have the (foolish) intention of taking on Amazon. Finally, even Wal-Mart could counter-attack: after all, as described by Erik Brynjolfsson and Andrew McAfee in a 2008 Harvard Business Review article, in the digital economy

an innovator [= Amazon] with a better way of doing things can scale up with unprecedented speed to dominate an industry. [But] in response, a rival [= Wal-Mart] can roll out further process innovations throughout its product lines and geographic markets to recapture market share. Winners can win big and fast, but not necessarily for very long.

A Reenactment of the Wal-Mart Effect?

9/ Wal-Mart was long considered an exceptional company: it earned a lot of money, served its customers exceptionally well, embodied proud American values, turned every member of the Walton family into a billionaire, created lots of jobs all around America, and even helped maintain inflation at a record-low level. Yet in 2005, Charles Fishman published his best-selling book The Wal-Mart Effect, in which he described in great detail how Wal-Mart also contributed, at its unusually large scale, to the relocation of American businesses overseas, a lowered quality of manufactured goods consumed in the US, and the frightening economic inequalities that are still crippling the US economy as of today.

For those who don’t know the story well, Sam Walton entered the retail store business in 1945, then opened his first retail store in Rogers, Arkansas, around 1950. Wal-Mart’s headquarters are still around today in Bentonville, Arkansas, even though the company quickly outgrew its roots: it now employs more than 1.5M people, which makes it still the largest corporate employer in the world.

Wal-Mart became one of the first big corporations to use digital technologies at a large scale. They collected vast amounts of data in their many stores and used them intensively to make their operations more efficient and force their suppliers to lower their prices. Wal-Mart ultimately grew so big, in no small part thanks to its information system, that it transformed the American economy. The infamous “Wal-Mart Effect” involves both good and bad features: lower prices for consumers, but also lower wages for workers and an unbearable pressure on suppliers.

A large part of Amazon’s history could have been predicted by those who already studied Wal-Mart. Like Wal-Mart, it is an uncommon company that achieves superior performances and creates a lot of value for both its stakeholders and the economy as a whole. But like Wal-Mart, it inspires more and more doubts as to the real amount of good that it does for society.

Amazon resembles Wal-Mart in so many ways. It grows at an exponential pace. Customers are its priority, and the CEO makes sure it stays that way. Most Amazon executives are Wal-Mart veterans, notably former CIO Rick Dalzell. It uses digital technologies extensively. And it has an ambivalent effect on the economy: schizophrenic consumers enjoy the convenience, wide choice, and lower prices, but many worry about Amazon’s formidable economic power over other players. Isn’t the company too hard on its workers? Can its suppliers stand the pressure of ever-decreasing cost of sales? Is Jeff Bezos a bad person?

Most questions lead to a discussion of antitrust policy. Should the government be harder on Amazon? It appears difficult: according to a tradition dating back to Ralph Nader, antitrust authorities have but one mission in a complex economy: defend the consumer’s interest. What if a company becomes dominant in the consumer’s best interest, what Peter Thiel calls a “creative monopoly”? Antitrust rules tend to become irrelevant in the face of such monopolies. And Amazon itself makes every effort not to turn into a predator in too visible of a way: for instance,Netflix is one of AWS’s most important customers, even though Netflix is also a direct (and tough) competitor to Amazon’s Prime Instant Videostreaming offer.

So far, just like Wal-Mart, Amazon proves that on a highly competitive market, customers beat workers and society most of the time — much to the displeasure of people like George Packer, who wonders if Amazon is good for books and reading in general, or Franklin Foer, who wrote in the New Republic that

if we don’t engage the new reality of monopoly with the spirit of argumentation and experimentation that carried [Supreme Court Justice Louis] Brandeis, we’ll drift toward an unsustainable future, where one company holds intolerable economic and cultural sway. Unfortunately, a robust regulatory state is one item that can’t be delivered overnight.

Today, Wal-Mart is still a formidable player. But it’s suffering, not only because Charles Fishman’s book has nurtured an ongoing public discussion about the “Wal-Mart Effect”, but also because the digital economy gave birth to new, more aggressive competitors, among them the mighty Amazon. The way Wal-Mart used to treat its employees has backfired. The pressure it exerts on suppliers has alarmed trade organizations, politicians, and the press. To try and solve these unprecedented problems, Wal-Mart decided to drop its “Lower Prices” taglinein favor of the more society-friendly “Save Money, Live Better”. Even more unexpectedly, it has decided to raise the wages of its 500,000+ employees, thus contributing to a national debate around the minimum wage. Will Amazon preemptively follow this path to escape Wal-Mart’s misguided ways ?

An Heir to the Dotcom Bubble

10/ Amazon is more than 20 years old. It was founded even before theNetscape IPO, the very event that launched the dotcom bubble in 1994. In that extraordinary context, it was easy for Amazon to raise capital, deploy its infrastructure and conquer its market. From its IPO in 1997 to its first (slightly) profitable year in 2003, Amazon burned through 3 billion dollars! This is the amount you have to invest to deploy such a large hybrid infrastructure. Raising that kind of money would be very difficult in today’s public market. But thanks to its early start and easy access to capital, Jeff Bezos is now to the digital economy what Cornelius Vanderbilt was to the railroad economy and Andrew Carnegie was to the steel-powered heavy engineering economy.

This is one of the counter-intuitive effects of bubbles. The economy always takes a hit when a bubble bursts. But, as we arereminded by William Janeway, some bubbles nonetheless contribute to value creation, particularly when they enabled the financing of assets that would never have existed if investors hadn’t been irrationally exuberant. The dotcom bubble in the 1990s created many such assets: giant infrastructures such as the Internet or the opening of military satellites to civil applications; technological assets such as open source software; and of course giant companies that survived and went on to play a key role in the rise of the post-bubble digital economy. As J. Bradford DeLong wrote in Wired more than 10 years ago, we’re witnessing a pattern that has existed in every technological revolution:

British investors in US railroads during the late 19th century got their pockets picked twice: first as waves of overenthusiasm led to overbuilding, ruinous competition, and unbelievable (for that time) burn rates, and second as sharp financial operators stripped investors of control and ownership during bankruptcy workouts. Yet Americans and the American economy benefited enormously from the resulting network of railroad tracks that stretched from sea to shining sea. For a curious thing happened as railroad bankruptcies and price wars put steady downward pressure on shipping prices and slashed rail freight and passenger rates across the country: New industries sprang up.

Therefore this last note is not so much a lesson to draw as it is a reminder of the extraordinary circumstances that surrounded the founding of Amazon. Many things have changed since, notably the fact that technology has been commoditized (including by Amazon Web Services) and that it is now cheaper than ever to start a digital company. But for all of you who would like to reenact Jeff Bezos’s prowess, remember that it demands taking bold risks and, at some point, raising a lot of money.

These Go to Eleven

11/ The gigantic, public, and secretive Amazon is one the digital companies that is the most covered by the media as well as by financial analysts and by numerous bloggers, among them many former Amazon employees. Here is a selection of preferred online publications, most of them widely used to prepare this double issue:

- Tim O’Reilly, “Open Source Paradigm Shift”, 2004.

- Meredith Levinson, “Amazon’s IT Leader Leaving Huge Customer Service Infrastructure as Legacy” (an article about Rick Dalzell), CIO, 2007.

- Jeff Bezos, “2010 Letter To Amazon Shareholders”, 2010.

- Steve Yegge, “Stevey’s Google Platforms Rant”, 2011.

- Farhad Manjoo, “I Want It Today: How Amazon’s ambitious new push for same-day delivery will destroy local retail”, Slate, 2012.

- The Economist, “Another Game of Thrones: Google, Apple, Facebook and Amazon are at each other’s throats in all sorts of ways”, 2012.

- Benedict Evans, “Amazon’s Profits”, 2013.

- Eugene Wei, “Amazon and the ‘profitless business model’ fallacy”, 2013.

- Justin Fox, “At Amazon, it’s All About Cash Flow”, Harvard Business Review, 2014.

- Philip Evans & Patrick Forth, “Borges’ Map: Navigating A World of Digital Disruption”, BCG Perspectives, 2015.

- Marcus Wohlsen, “Amazon Prime Is One of the Most Bizarre Good Business Ideas Ever”, Wired, 2015.

(This is an issue of The Family Papers series, which is published in English on a regular basis. It covers various areas such as entrepreneurship, strategy, finance, and policy, and is authored by The Family’s directors as well as occasional guest writers. Thanks to Kyle Hall, Balthazar de Lavergne, and Laetitia Vitaud for reviewing drafts. This story was originally divided in two, but both parts have been reunited here—the former part 2 being kept on Medium in order to preserve readers’ comments and annotations.)